A bill of sale is a document that proves the transfer of ownership of a good or asset from one party to another. It's a crucial piece of paperwork that protects both the buyer and seller.

In the United States, a bill of sale is often required by law for certain types of transactions, such as the sale of a vehicle or a boat. This helps to ensure that both parties are aware of the terms of the sale and can provide evidence of ownership.

A well-written bill of sale can also help to avoid disputes and confusion down the line. By including all the necessary details, such as the asset's description, purchase price, and any warranties or guarantees, a bill of sale can provide a clear and transparent record of the transaction.

Here's an interesting read: Real Estate Asset Management Companies

What is a Bill of Sale?

A bill of sale is a legal document that records the transfer of ownership of goods or property from one person (the seller) to another (the buyer). It's a contract that formalizes the transfer of assets between two parties.

Most states require a bill of sale as proof of purchase when buying or selling a vehicle or a branded animal, like a horse. This is to ensure that the ownership is properly transferred and documented.

A bill of sale is commonly used when selling or buying an item of value. It's essential to use one to avoid any potential disputes or issues in the future.

Here are the main purposes of a bill of sale:

- Documents the transfer of ownership

- Records the sale price

- Documents the sale terms and conditions

An absolute bill of sale is used when a good is paid for in full and in "as is" condition. This means that the buyer has paid the full amount and is taking the item as is, with no warranties or guarantees.

A conditional bill of sale, on the other hand, is used when conditions need to be placed on the buyer's ownership. This could include requirements for the buyer to notify the seller in the event they plan to resell the item.

Types of Bills

A bill of sale is a document that transfers ownership of goods or property from one person to another, but did you know that there are different types of bills of sale? Each type serves a specific purpose, and understanding them is crucial to ensure a smooth transaction.

Some states have different requirements for bills of sale, so it's essential to check local guidelines.

There are several types of bills of sale, including Absolute, Conditional, Quitclaim, and Vehicle Bills of Sale. The type of bill of sale used depends on the circumstances of the sale.

An Absolute Bill of Sale is the most basic type, where the seller transfers ownership to the buyer without any conditions or warranties. It's commonly used for everyday transactions, such as selling personal items or transferring ownership of vehicles with no outstanding loans or liens.

A Conditional Bill of Sale is used when the seller is using the goods as collateral for a loan. If the debtor fails to pay back the loan, the creditor can take possession of the goods.

Explore further: Types of Real Estate Investment Trusts

A Quitclaim Bill of Sale is used when the seller is unsure if they own the property or doesn't want to warrant the title. This type of bill of sale is often used in situations where the seller is unsure of their rights to the property.

A Bill of Sale with Warranty guarantees that the seller owns the property and has the right to transfer it. This type of bill of sale provides more protection for the buyer.

Here are some common types of bills of sale:

- Absolute Bill of Sale: Transfers ownership without conditions or warranties.

- Conditional Bill of Sale: Used when the seller is using the goods as collateral for a loan.

- Quitclaim Bill of Sale: Used when the seller is unsure if they own the property.

- Bill of Sale with Warranty: Guarantees that the seller owns the property and has the right to transfer it.

- Vehicle Bill of Sale: Required in some states, but not all, to transfer ownership of a vehicle.

Essential Elements

A well-structured Bill of Sale is essential for correctly and legally recording the transfer of ownership. It's a tangible piece of evidence that provides clarity and documentation of the transaction.

A Bill of Sale acts as proof of ownership for the buyer, protecting them from potential claims by third parties. This is especially important in post-transaction disputes or disagreements.

Here are the vital aspects to include in a thorough Bill of Sale:

- Legal Clarity and Documentation

- Proof of Ownership

- Liability Protection

These essential elements ensure that both the buyer and seller are protected, making the transaction smooth and hassle-free.

Describe the Item

Describing the item is a crucial part of a bill of sale. It's what sets it apart from a receipt.

To provide enough detail, start by listing the make, year, and model of the item, if it's a tangible object. This is especially important when selling a car, where you'll also include the Vehicle Identification Number (VIN) and mileage.

The level of detail will vary depending on the item's complexity. For instance, if you're selling a piece of equipment, you'll include its make, year, and serial number. This ensures the buyer has all the necessary information to confirm the item's authenticity and functionality.

While it may take some time to gather this information, it's worth the effort to avoid any potential disputes or misunderstandings down the line.

Legal Clarity

A well-structured Bill of Sale is key to avoiding potential disputes and ensuring a smooth transaction.

Including the date of purchase in a Bill of Sale is crucial, as it provides a clear record of when the transaction took place.

In many states, only the buyer is required to sign the document, making it essential to check your state's specific requirements.

A generic Bill of Sale typically includes the names and addresses of both the seller and the buyer, which helps prevent any confusion or disputes.

The signatures of both the seller and the buyer are also essential, as they confirm the agreement and transfer of ownership.

Here are the essential elements of a Bill of Sale that provide legal clarity:

A Bill of Sale acts as tangible evidence of a transaction, providing legal clarity and documentation of ownership transfer.

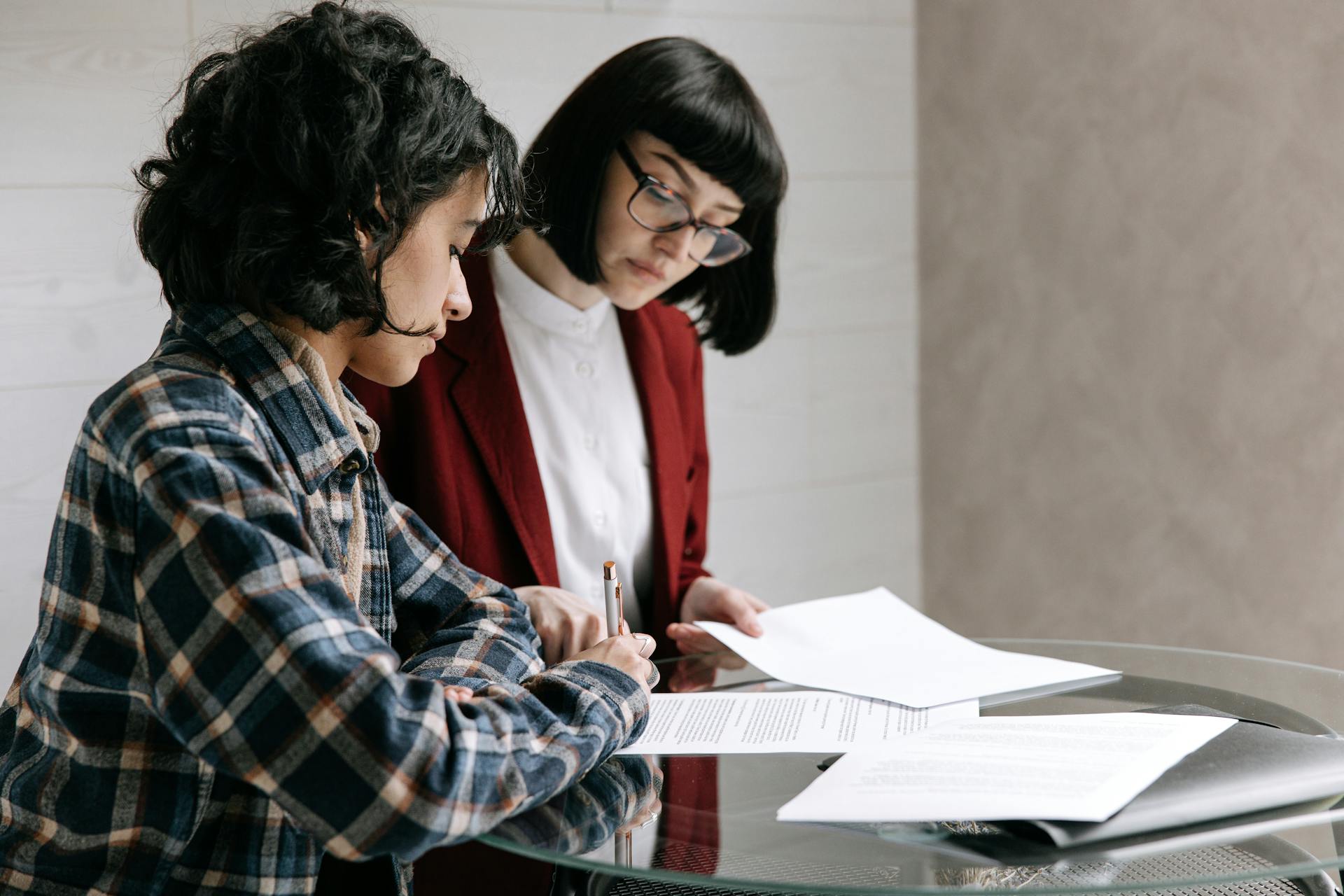

How to Write a Bill of Sale

To write a bill of sale, the seller is responsible for drafting the document, which should include the seller's name and address, the buyer's name and address, and a description of the item being sold. The document should also include the vehicle identification number if it's a vehicle sale.

Suggestion: Solo 401k Plan Document

The bill of sale must contain certain information to be legally binding, including the seller's name and address, the buyer's name and address, a description of the item being sold, the date of transaction, the amount paid, and the method of payment. It's a good idea to use a template or form to make the process easier.

Here are the essential elements to include in a bill of sale:

- Seller's name and address

- Buyer's name and address

- Description of the item being sold

- Date of transaction

- Amount paid

- Method of payment

Identify Items for Sale

Identify the item(s) you're selling. Exactly what you're selling will dictate the information listed in your bill of sale.

The type of item you're selling will influence the details you need to include. For example, selling a vehicle requires different information than selling several unneeded computers.

You can include multiple items on a single bill of sale, but it's up to you to decide what's best. Simply list out the items and their associated costs on separate lines.

However, if your items have different payment methods, payment terms, or information like loans or liens, it's probably worth breaking them out into separate bills of sale to avoid confusion.

You might enjoy: Online Bill Payments

5. Payment Details

When writing a bill of sale, it's essential to include the payment details. The selling price of the item should be clearly stated.

The payment method, whether it's cash, check, credit card, or something else, should also be specified. This information is crucial for both the buyer and the seller to keep track of the transaction.

The bill of sale should clearly answer the following questions:

- What is the selling price of the item?

- Is the payment in installments or paid in full?

- What method is the payment made in (cash, check, credit card, etc.)?

This information will help prevent any misunderstandings or disputes down the line.

How to Write

Writing a bill of sale is a straightforward process, and I'm here to guide you through it. The seller is responsible for drafting the bill of sale, so make sure you're the one creating it.

You can find free bill of sale templates online to make the process easier. Some popular options include Free Forms, LegalContracts.com, and LegalTemplates. These templates can save you time and effort.

To write a bill of sale, you'll need to include certain information. This includes the seller's name and address, the buyer's name and address, a description of the item being sold, and the date of transaction. The previous owner, amount paid, method of payment, and any agreements regarding due dates for pending payments should also be included.

See what others are reading: Bank Owned Homes Free Listings

Here are the key pieces of information you should include in a bill of sale:

- Seller's name and address

- Buyer's name and address

- Description of the item being sold

- Date of transaction

- Previous owner

- Amount paid

- Method of payment

- Any agreements regarding due dates for pending payments

Double-check your bill of sale to ensure all the information is correct and there are no mistakes.

Fill Out the Document Accurately

Start by giving your bill of sale a clear title, such as "Bill of Sale." This will help both the buyer and the seller understand the purpose of the document.

The parties involved should be listed, including the full names and addresses of both the buyer and the seller. Make sure to enter the details accurately to avoid confusion or disputes.

A detailed description of the item or property being sold is crucial. Include all identifying information, such as the make, year, and serial number, to ensure the buyer knows exactly what they're getting.

The sale price should be clearly stated, both numerically and in words, to avoid any confusion. Ensure that the numerical and written prices are consistent.

Here's an interesting read: How to Avoid Masshealth Estate Recovery

Specify the agreed-upon payment terms, including any down payments or installment schedules. This will help both parties understand the terms of the sale.

Enter the date of the transaction and the location where it occurred. This will provide a clear record of the sale.

Include spaces for the signatures of both the buyer and the seller. Ensure that both parties sign the document in the presence of witnesses, if required by local regulations.

Here are the essential details to include in your bill of sale:

When to Use a Bill of Sale

A bill of sale is commonly used when selling or buying an item of value. This is why most states require a bill of sale as proof of purchase when buying or selling a vehicle.

You can use a bill of sale when buying or selling a vehicle, or a branded animal like a horse. If you're the buyer, you can even bring one with you to the transaction.

The bill of sale is essential in the world of autos, where it keeps track of the sales of automobiles, motorbikes, boats, and other vehicles. It's also used in real estate transactions, personal property sales, business asset transfers, livestock and agricultural sales, and even art and collectibles.

Common Uses Across Industries and Transactions

A bill of sale is a versatile document that can be used in various industries and transactions. It's essential for vehicle sales, keeping track of sales of automobiles, motorbikes, boats, and other vehicles, and establishing proof of ownership transfer.

In real estate transactions, a bill of sale can be useful to record the transfer of personal property, such as appliances, furniture, or fixtures. This ensures that both parties are on the same page.

Personal property sales, like buying and selling gadgets or furniture, can also benefit from a bill of sale, defining the conditions of the sale and what's included in the purchase. This protects both parties involved.

Business asset transfers, such as documenting the transfer of equipment, inventory, or intellectual property, can be facilitated with a bill of sale. This ensures a smooth transition of assets.

In the agriculture sector, a bill of sale is used to record the sale of animals, machinery, and crops, guaranteeing that the specifics of the transaction are formally documented. This is crucial for farmers and ranchers.

Art & Collectibles also rely on bill of sales to authenticate the authenticity and ownership of high-value objects, such as artwork and collectibles. This provides peace of mind for both buyers and sellers.

For another approach, see: Home Ownership Equity Protection Act

When to Use It

A bill of sale is a crucial document that proves ownership of an item, and it's essential to know when to use it.

Most states require a bill of sale when buying or selling a vehicle or a branded animal, like a horse. This is a common requirement in many states to ensure a smooth and legal transaction.

You can use a bill of sale for everyday transactions, such as selling personal items like furniture, electronics, or appliances. This type of transaction is perfect for an Absolute Bill of Sale, which denotes the seller's complete transfer of ownership to the buyer.

A bill of sale is also necessary for complex transactions, like selling vehicles with no outstanding loans or liens. This document provides numerous legal and financial benefits to both purchasers and sellers.

Some common examples of transactions that require a bill of sale include:

- Selling personal items, such as furniture or electronics

- Transferring ownership of vehicles

- Simple exchanges of personal property

In summary, a bill of sale is a vital document that proves ownership of an item, and it's essential to use it for various transactions, including buying or selling vehicles, branded animals, or personal items.

Legal Compliance

In many jurisdictions, using a Bill of Sale is not just a good idea, it's a requirement. Failure to use one when necessary can result in legal implications.

Specific transactions require a Bill of Sale to be legally valid, so it's essential to check local and state/country regulations before making a sale. Using a Bill of Sale ensures compliance with these regulations, preventing potential legal issues and fines.

A Bill of Sale makes the terms of the transaction legally enforceable, protecting the interests of both parties involved. This is crucial for preventing disputes and ensuring a smooth transaction.

Here's a breakdown of the benefits of using a Bill of Sale for legal compliance:

- Legal Compliance: Using a Bill of Sale ensures compliance with local and state/country regulations, preventing potential legal issues and fines.

- Enforceability: It makes the terms of the transaction legally enforceable, protecting the interests of both parties.

Benefits and Importance

A bill of sale is a crucial document that provides evidence of ownership transfer, and it's a small price to pay for the peace of mind it gives both the buyer and seller.

Creating a bill of sale takes just 10 minutes, but it can save you from potential disputes and problems down the line. It's a worthy investment that's essential for any larger item sale.

In some states and situations, a bill of sale is even required to certify ownership and complete the sale of a vehicle. This ensures you're abiding by regulations and avoids any fees, problems, or penalties.

Here are the key benefits of a bill of sale:

- Provides evidence of ownership transfer

- Ensures compliance with state regulations

- Aligns expectations between buyer and seller

Benefits

Creating a bill of sale offers several benefits that can give you peace of mind and protect your interests. Providing evidence of ownership is one of the main advantages, as it proves that you've transferred ownership and the buyer is the new owner.

A bill of sale helps you stay compliant with local regulations. In some states, it's required to certify ownership and complete the sale of a vehicle, and drafting the bill of sale ensures you're abiding by these regulations.

Having a bill of sale can also help prevent disputes by aligning the expectations of both the buyer and seller. They'll review and sign the document, confirming their understanding of the item's details and condition.

Here are the key benefits of using a bill of sale:

- Provides evidence of ownership

- Helps you stay compliant with local regulations

- Aligns the expectations of both buyer and seller

Drawing up a bill of sale is a worthwhile investment of your time, taking only around 10 minutes to complete.

Importance of Translation

Translation is a crucial aspect of Bill of Sale transactions, particularly in international deals where language barriers can cause confusion. Clarity and understanding are ensured when a Bill of Sale is translated, reducing the risk of conflicts and misunderstandings.

Transactions involving partners who don't speak the same language require translation to avoid miscommunication. In some jurisdictions, legal papers like Bills of Sale must be translated into specific languages to meet official standards.

International transactions often involve translating a Bill of Sale into the foreign party's language, making the transaction legitimate and enforceable. This practice has become common in a globalized society where commercial transactions cross borders frequently.

Writing and Signing a Bill of Sale

The seller is responsible for drafting the bill of sale, which should be signed and dated by both the seller and buyer to make it official.

A bill of sale is a formal document that brings clarity and formality to a sale, and it's not that challenging to create one.

Intriguing read: Seller Financing Addendum

To write a bill of sale, you can use a free template from websites like Free Forms, LegalContracts.com, or LegalTemplates.

Six steps can help you figure out how to write a bill of sale, including including a description of the item being sold, the date of transaction, and the amount paid.

You should also include space for signatures at the bottom of the document where both parties can sign and finalize the deal.

The bill of sale must contain information such as the seller's name and address, the buyer's name and address, a description of the item being sold, and the amount paid.

To make sure all the information is correct, it's a good idea to re-read and double check your bill of sale, and consider contacting a business lawyer if you have any questions.

Signatures from both the buyer and seller are necessary, and providing a spot for witnesses to sign is also a good idea, although not always necessary.

Notarization by a notary public may be required depending on the nature of the transaction and local legislation, adding an extra degree of credibility to the document.

Readers also liked: Why Flipping Houses Is a Bad Idea

Here are the essential components of a bill of sale:

After completing these steps, you'll have a fully executed bill of sale that serves as a legally enforceable document, certifying ownership transfer and defining the terms of the transaction.

Protecting Against Fraud

A Bill of Sale is a powerful tool in preventing fraudulent activities. It clearly documents the details of the sale, discouraging dishonest practices.

By writing down the terms of the sale, you're creating a paper trail that can be used to verify the transaction. This reduces the risk of post-sale disputes regarding the item's condition.

A Bill of Sale also allows for verification of the item's condition at the time of sale, reducing the chance of disputes.

Frequently Asked Questions

Is a handwritten bill of sale legit?

A handwritten bill of sale is a legitimate way to transfer ownership, especially when verified by a notary witness. It's a traditional method that can be just as secure as a printed document.

Featured Images: pexels.com